When the COVID-19 pandemic began to reshape business operations globally, the preliminary response of CEO’s, CFO’s, and Treasurer’s was all about survival of their business: free up cash, liquidity (working capital), and resources to keep their business operations afloat.

Due to the economic fallout, many organisations experienced devastation with their business operations and all due to inadequate cash resources. This severely impacted their Balance Sheets, and they were forced to review their cash-flow, but with the immediate need to preserve cash reserves. Thereby, making drastic changes and enforcing mandatory cuts across the enterprise on capital expenditure, dividends, reductions in expenses (and discretionary spending), and temporary business / plant closures.

In hindsight, what the COVID-19 pandemic highlighted was a key lesson and the critical importance of ‘best practice’ principles for safeguarding cash and liquidity management. The unfortunate timing has now created an incredible opportunity for CEO’s, CFO’s, and their Executive Management Teams to elevate their cash-management capabilities; by redirecting their focus from “cash preservation” to “cash excellence”.

What is Working Capital Management?

Working Capital Management is the most significant and critical component for the financial health of any organisation. It can improve a company’s cashflow management and earnings by using its resources efficiently. Also, it refers to an organisation’s strategy (and focus) on monitoring and utilising the two (2) components of Working Capital — Current Assets and Current Liabilities.

Working Capital (also known as Net Working Capital) is the money that an organisation has on hand to pay short-term expenses and liabilities. Working Capital is composed of Current Assets that will be available for use by an organisation, within the next twelve (12) months. These assets can include:

- Cash

- Accounts Receivable

- Marketable Securities

- Inventory

- Other Liquid Assets

Businesses use Working Capital to cover Current Liabilities, or those debts and expenses that a company is responsible for over the next 12 months. These liabilities can include:

- Accounts Payable

- Payroll

- Loan Interest Payments

- Debt Payments

- Tax Obligations

Working Capital Optimisation: Why is it important?

The primary purpose of Working Capital Optimisation is to ensure that an organisation maintains sufficient cashflow to meet both its short-term operating costs and its short-term debt obligations.

But Working Capital Optimisation is often hard to get right. It requires significant cross-functional efforts (led by your Executive Team) across the entire organisation and to execute its objectives effectively. However, it is often one of the cheapest ways to obtain ’free’ cash for an organisation, adds value to all stakeholders (inc. shareholders), and is considered of strategic importance for the entire business, not just the Finance function.

There are three (3) fundamental components for effective cash management, and all must be tightly integrated to maximise cashflow benefits.

Working Capital Optimisation

To simultaneously manage elements of the Balance Sheet and P&L Statement in an integrated fashion by accelerating the conversion of operating Working Capital into Cash and managing Expenses.

Effective Working Capital Management requires a strategy that focuses on business performance because releasing excess levels of cash (tied up in Working Capital) represents the cheapest form of finance. There is no requirement to procure finance options (last option) but how to access more cash, by unlocking your ‘free’ cash. The three (3) components are as follows:

Order-to-Cash (O2C) – Accounts Receivable

The main objective is to reduce the Accounts Receivable balance to release tied-up capital. This can be achieved by a more systematic collections process, predictive metrics to target slow payers, robust disputes management, standardise payment terms, or the use of invoice financing methods.

Procure-to-Pay (P2P) – Accounts Payable

The main objective is to increase external financing for Accounts Payable, whilst also taking advantage of discount options (% for early payment). The preferred option is to extend payment terms and purchasing conditions, but this is heavily dependent on the negotiating power of the organisation to help sustainably reduce process costs.

Forecast-to-Fulfil (F2F) – Inventory

Inventory represents a critical target metric for optimising working capital. All process improvements are aimed at reducing inventory levels and without causing disruptions in supply (to customers) at the same time. But it is particularly important to emphasise that disruptions along the entire organisation’s supply chain, also has a direct impact on financial processes.

Cashflow Forecasting

Leveraging the knowledge from Working Capital Optimisation together with other cash management activities to forecast ‘cash cycles’ and to predict the organisation’s needs (and surpluses) with metrics.

Treasury and Finance Teams use Cashflow Forecasting to guide daily funding and risk management decisions, while also feeding data analytics into critical reporting processes. However, measuring the accuracy of cash forecasts for decision making reporting purposes (on an ongoing basis) is critical to operating a high-value Cashflow Forecasting process.

Liquidity Management

Leveraging the knowledge from Cashflow Forecasting together with investing and financing strategies to maximise the return on cash generated, and the balance of Liquidity Management can be measured by an appropriate level of cash reserves. It is the organisation’s ability to quickly (and efficiently) generate more cash resources to finance its business needs; both short-term and long-term.

Managing liquidity ensures that the organisation has enough cash resources for its ordinary course of business and unexpected needs (reasonable cash reserves). Why is this important? Well, because it affects an organisation’s creditworthiness, which can contribute to whether the business is either a success or failure.

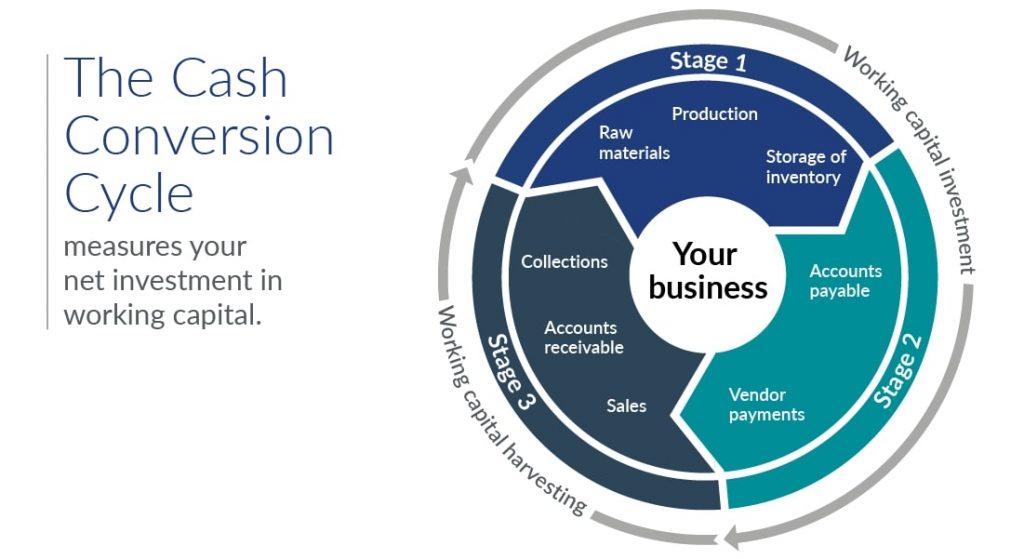

The critical value of the Cash Conversion Cycle (CCC)

The Cash Conversion Cycle (CCC) simply measures how efficiently any organisation’s management is managing its Working Capital. The Cash Conversion Cycle (CCC) is a Working Capital metric which measures how many days it takes an organisation to convert cash into inventory, and then back into cash via the sales process. The shorter the value of an organisation’s Cash Conversion Cycle (CCC), the less time that cash is ‘trapped’ in its operations within Accounts Receivable and Inventory.

Cash Conversion Cycle (CCC)

- CCC uses DSO, DPO and DIO to demonstrate how effective a company is at managing its short-term assets and liabilities.

- CCC is a key indicator of Working Capital Management efficiency.

- CCC = DSO + DIO – DPO.

DSO (Days Sales Outstanding)

- DSO shows how long it takes to collect cash from customers.

- Faster sales collections have a positive Working Capital impact.

- DSO = (Av. Accounts Receivable amount in a given period / Total Credit Sales in the same period) x Number of Days in the Accounting Period (refer Accounting Timetable).

DIO (Days Inventory Outstanding)

- DIO shows how quickly inventory is sold.

- Selling stock faster has a positive impact on Working Capital, as it means that cash is ‘trapped’ in unsold goods or inventory.

- DIO = 365 Days / Inventory Turnover (COGS / Av. Inventory Balance for Period).

DPO (Days Payables Outstanding)

- DPO shows how long it takes to pay suppliers.

- Longer payment durations have a positive impact on Working Capital.

- DPO = (Av. Accounts Payable / Cost of Goods Sold) x Number of Days in the Accounting Period (refer Accounting Timetable).

The liquidity of any organisation (small business, SME, or Enterprise) can be ‘trapped’ in each of the above areas, including processes. Effectively, the cash is ‘trapped’ and cannot be used for other purposes (time), as it is moving through the entire supply chain process.

But how can you avoid this situation? Well, to accelerate cashflow, it is a very straightforward process – decrease DSO, decrease DIO, and increase DPO – and all items contribute to lowering the value of the Cash Conversion Cycle (CCC).

Summary

Working Capital Optimisation is the cheapest way to free up cash in any organisation. A strategic approach to Working Capital Management should include your key initiatives within Accounts Receivable, Accounts Payable, and Inventory.

Leveraging effective Working Capital Management processes through each of these three (3) components can maximise cashflow, yield substantial returns, reduce risks, and costs. But the challenge to growing businesses with high sales and increased expenses, places a massive strain on cashflow and offsets the balance(s) of Working Capital.

Working Capital strategies that involve performance metrics, KPI’s, benchmarks, and accountable people drives a business to achieve long-term success. Effective Working Capital Management improvements are the key to generate more cash for a business, increase operational efficiency, raise profitability, and potential growth.

This article was a Guest Author contribution and collaboration with CreditorWatch.

Need some guidance on your next steps? Let’s start a conversation…